Were We Wrong About Park Owned Homes?

Everybody loves the “parking lot” MHP.

The 100% tenant-owned park with that sweet, consistent and highly profitable lot rent.

Ain’t nobody loving park owned homes.

Well, at least that has been the prevailing sentiment for 50 odd years.

But, life happens:

you inherit some homes when tenants skip town

you buy a few homes to fill vacant pads

you buy that 100% rental park in South Carolina because “the demographics look unreal”

And soon enough, you’re a trailer mogul!

You can now impress people at parties. Instead of, “I own manufactured home communities”, which gets blanks stares and the occasional, “oh, you mean trailer parks”…

...you can now say “I own 250+ rental homes” (cough: “single-wides”)

Anyways, it’s hard to stay out of the park owned home game these days.

But maybe, just maybe…the home business isn’t all that bad.

Home Sales

What if owning the homes was part of a LARGE home sales business.

How does the largest MHP operator (SUN Communities) do with park owned homes?

SUN Communities 2022 Annual Report Excerpt:

(their 2023 annual report hasn’t ‘dropped’ yet)

SUN sold $126mm of new homes in 2022 for a record ~$180,000 a mobile home!

So their average new home is more valuable than most Louisiana MHPs.

Plus, they sold another $149mm of used homes at roughly $60K per home.

Man these sound expensive, but this is where the industry is heading…eventually.

MHP housing stock needs to be upgraded. I suspect that at some point lenders (namely Fannie Mae) will require it, but I digress.

The average monthly rental rate for these homes was $1,221 - a healthy ~10% increase over 2021.

You might have noticed that SUN appears to be netting an impressive 18% margin on new home sales and a whopping 45% on used homes!

In total, SUN made an extra ~$90,000,000 in 2022 just from home mark-ups.

Now, this is gross margin, so we have to deduct selling expenses (staff + marketing) to sell these homes. SUN says that was ~$7mm, which makes their total “NOI” from home sales about $83mm.

I would also guess their used home mark up isn’t pure margin as perhaps the book value of those homes was depreciated. However, I’m probably just jealous and nitpicking.

Anyway you slice it, home sales appears to be a good business.

Okay, that’s sales, what about park owned home rental operations?

Surely that business stinks?

Think again!

81% margins!!

WHAT?!

These numbers are not computing for me.

Needless to say, my experience with POH margins has been…well, different.

Maybe there is some accounting mumbo jumbo going on in these numbers.

Maybe they are combining lot rent + home rent as their denominator vs. just home rent (seems likely, but still impressive).

Maybe I’m missing something buried in disclosures.

Maybe I’m an idiot.

Rant over?

Nope!

For all we know they’re capitalizing every minor repair (i.e. moving expenses off the income statement to the balance sheet, which artificially boosts profit margins).

CFO: “What’s this home repair line item on the income statement?”

Bookkeeper: “We fixed a janky toilet.”

CFO: “That’s an investment, capitalize that baby!”

Man, I don’t know, but park owned homes sure seem profitable for SUN.

This is probably why they own a lot of homes.

Getting close to 10,000 park owned homes.

Can you imagine their poor home title department? No offense to any readers that work in the back office, you guys rock but…

I wouldn’t wish that job (chasing down MH titles all day) on my worst enemy.

Also notice the 640 rental homes Sun sold in 2022.

This rental conversion is a critical part of their home program. They reach out to rental tenants periodically with sale offers.

This is keeping their POH ratio (POHs to total MH sites) in check. It’s currently about 8% of their total sites.

I know other (smaller) firms that have gone full-tilt on rentals, aka the “horizontal apartment” approach.

Without a conversion program, those firms POH ratio keeps ballooning. This should work…until it doesn’t.

Park Owned Home Circle of Success

However, if you can use park owned homes to:

infill vacant pads

upgrade the housing stock and appearance of the park

earn huge NOI margins on the rentals

then methodically go back each year to sell a sizable % of those rentals

All while clipping a chunky 18% - 40% profit margin over invoice….

Then you should LOVE the parked owned business.

But maybe SUN is an outlier.

What about Equity Lifestyle?

ELS 2022 POH Numbers:

POH Rental Margin: 87%

Damn.

It’s me. I’m the problem. It’s me.

I’ve never sniffed these numbers on POHs. Man I hope I don’t get a bunch of emails saying, duh…we all run 80%+ margins on used and new homes.

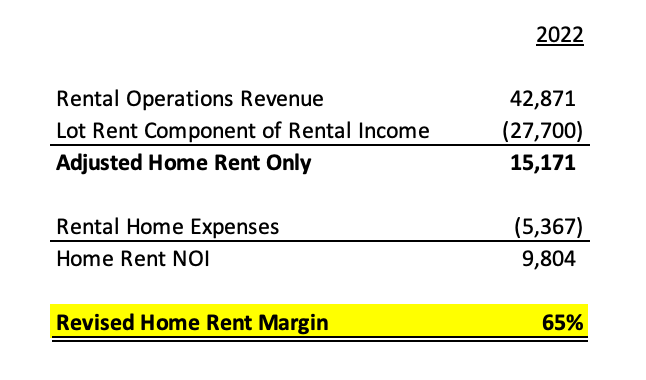

But wait. What about the above footnote!?

(1) Rental operations revenue consists of Site rental income and home rental income. Approximately $27.7 for the year ended December 31, 2022 of Site rental income is included in MH base rental income in the Core Portfolio Income from Property Operations

Okayyyyyy. Lot rent is included in ELS rental numbers.

Let’s pull out lot rent to reconcile that math.

I feel a bit better.

What might explain the delta between SUN & ELS? Well, as you can probably tell reconciling public company accounting is a nightmare.

Perhaps when the nerds (I say this lovingly) crank through all the GAAP adjustments, the actual cash margins are about the same. I’m not exactly doing forensic accounting here.

So what else might explain these juicy POH operating margins?

NEW HOMES + Scale

ELS owns 2,000 new rental homes out of their combined ~2,800 homes.

This makes a bit more sense to me as new home inventory is A LOT easier to maintain (higher quality tenant, fewer things breakdown, etc.)

Plus, the mega firms command large wholesale discounts from home manufacturers and probably buy the upgraded + most resilient homes.

Their parks are usually larger and are staffed by 5 star crews that keep supplies on hand and can crank through rental repairs fairly quickly + cheaply.

Smaller parks in small towns have to track down random contractors that have a tendency to disappear mid-job, leave fast food wrappers and empty Red-Bull cans everywhere then over-bill for repairs.

Rent-to-Own

ELS & Sun own a ton of 4+ star parks in strong, growing markets. It’s much easier to tie up capital in home inventory when those homes are not sitting on your balance sheet forever.

You can front the capital for new rentals when the buyer market is soft, but eventually market demand overwhelms home supply.

At which point you can push home rents faster than lot rents, which motivates the tenant to purchase their rental and you get those homes off the books.

Which is why the big firms don’t need to fool around with wacky “rent-to-own deals”. Rentals are fine because you have the operational skill, staffing, sales machine and demand to convert all POHs, eventually.

Where this hurts is when you’re in a softer market with no real team, maintaining a sea of park owned homes you can’t move, which you probably overpaid for in a park purchase.

You can try gimmicks like putting the homes on rent-to-own contracts - or worse Rent Credit Agreements - where you try to convince the renter they are racking up points for on-time rent payments.

This is the world’s least sexy rewards program.

It’s fun when you have one of these arrangements and the tenant constantly calls for point updates on their home.

Then there is the popular ‘Lease Option’ contract, where the option payment sure looks a lot like a downpayment.

These are all goofy. As you can probably tell, I’m not a fan. I don’t love seeing parks that have “no park owned homes” only to later find out they have:

12 rent credit agreements

25 lease options

and 5 promissory notes (yet title is still in the park’s name)

Newsflash: They Are All Rentals

I applaud the effort to incentivize tenants to feel like homeowners and take care of their space.

In soft markets, you have to try things to improve your odds of not getting back a trashed home 3 months after you just renovated it for $8,000. That hurts. You feel defeated when that happens.

Your mileage may vary, but I just never unlocked the “rent-to-own” code. In my experience, short of seeing their name on title, the tenant still thinks they’re a renter (and treats the house accordingly).

I’d still wager - and SUN & ELS numbers seem to support this - the most effective defense is higher quality homes, which only higher quality people can afford (I mean on average, don’t cancel me).

That might sound harsh, but if you’ve owned a bunch of old park owned homes you know this isn’t up for debate.

So Where Do We Shake Out on POHs?

POHs can be highly profitable if you line up these conditions:

A strong market with high average home prices

A park (or local portfolio) large enough to justify on-staff maintenance

Standardized repairs & regular maintenance schedules

Common repair materials stored onsite

Preventative systems (periodic walk throughs, smoke & carbon monoxide detectors tests and remote water meters - then jump on any water leaks

Use of maintenance software - or maintenance modules - in property management software to log a history of repairs

A proactive sales approach that pitches your best rental tenants each year on purchasing a home - show them the math on a proposal, bump the home rent slightly higher than lot rent (assuming the market supports the combined total of course).

Pony up for new, sturdy homes with material upgrades

In other words, POHs work best if you already have a big-boy operation with detailed systems and resources.

Until then, it’s a bit of a crapshoot so best not to go hog-wild on a POH strategy.

Happy Trails,

MHP WEEKLY