Our Favorite MHP Lady

My wife thinks I’m cheating on her.

She catches me in my sleep whispering sweet nothings to my dear, sweet Fannie Mae.

Aka, the Federal National Mortgage Association - the US sponsored agency and the largest lender to mobile home parks.

Now, I’m not actually fantasizing about a lender but I still like thinking of Fannie Mae as a kind and generous lady.

I asked AI what lender Fannie Mae might look like personified as a middle-aged woman and its rendition looks oddly appropriate….

Feels like she could fix the tractor, run a board meeting and then bake you a mean peach cobbler.

Ok, fine I admit it, this is getting weird.

Yet who else would give you tens of millions of non-recourse, interest only loans? Grandma? Hell no, Grandma grew up in the depression, she’s stingy. Plus she’s doesn’t have that kind of coin.

But Fannie does and she LOVES mobile home parks.

You can even call her out of the blue and get a supplemental loan with minimum paperwork and reduced transaction costs. CMBS lenders won’t even answer the phone.

Without her mobile home parks would be less “liquid” (fewer buyers) and less profitable.

Thank you Fannie Mae.

Fannie Mae Loan Stats

And apparently, Fannie knows what she’s doing. Entering the mobile home park lending business was a stroke of genius considering its lower risk profile.

Fannie Mae’s MHC book of business had a serious delinquency rate of only 0.12% as of June 2024.

That’s a rounding error barely worth mentioning compared to most real estate asset classes. It’s a fraction of Fannie’s apartment delinquency rate.

And this isn’t just the mega parks owned by the largest operators. While the average unpaid MHP principal balance was $11.2 million, 66% of all loans involved smaller properties (well, small for Fannie at less than $9M).

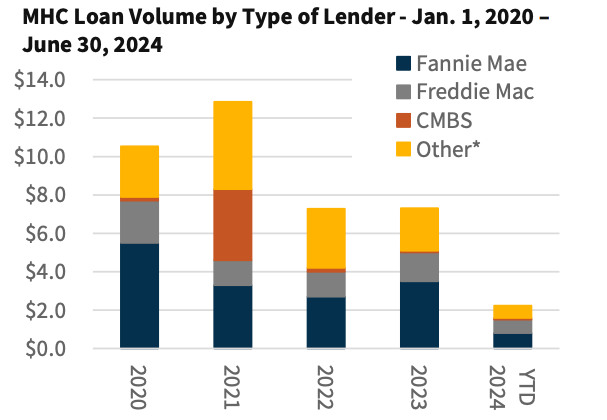

As of June 2024, Fannie Mae had financed 1,900+ MHC loans, covering over 750,000 sites, with a total unpaid principal balance of $22 billion.

Loan volume is still dramatically below peak MHC financing volume of $5.5 Billion in 2020. Fannie financed a much lower $800M in the first half of 2024.

Fannie’s Book of MHC loans only represents about 5% of its overall multifamily book of business. But the credit quality of that book is incredibly strong with an average DSCR (debt service coverage ratio) of 2.3x.

Short of a complete economic collapse, it’s hard to image how they’d see significant impairment from this loan book given that substantial margin for error. Especially considering the recession resistant rental stream and lower cap-ex costs to maintain parks.

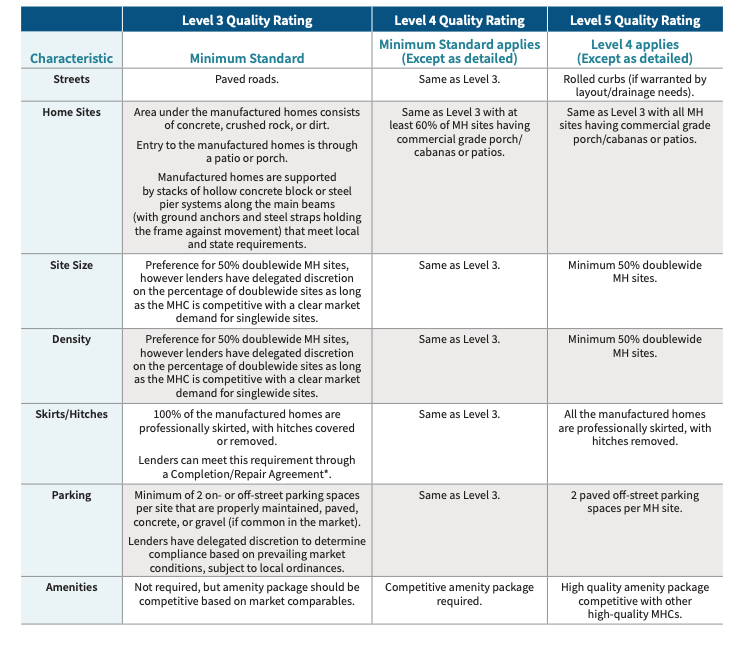

Park Criteria

To be considered for Fannie Mae financing, an MHC must meet specific property characteristics:

At least 50 sites

Paved roads throughout

Area under the homes can consist of concrete, crushed rock, or dirt

Homes properly set and anchored according to local requirements

100% of homes must be professionally skirted, with hitches must covered or removed (they are sticklers about hitches)

A minimum of 2 on or off-street parking spaces per site, properly maintained and paved, concrete, or gravel (if common in the market)

Amenities are not required at Level 3, but the amenity package should be competitive based on market comps

The MHC must achieve at least a Level 3 Quality Rating according to Fannie Mae's MHC Quality Rating Standards

MHC Quality Ratings

I’ve always felt the level or star rating system for mobile home parks was a bit arbitrary.

Whenever I’m asked, “can you define a three or four star park?” I feel like Supreme Court justice Potter Stewart when asked to define pornography…..

“I know it when I see it”.

Fannie Mae uses a five-level quality rating system, with Level 5 being the highest and Level 1 the lowest. This is basically the same as the 1-5 Star park rating convention most MHP investors reference.

Most properties in Fannie Mae's MHC loan portfolio are rated Level 3. Here is detailed table of their rating system if you want to geek out:

Or if you’re a visual learner:

MHP Market Plus Check

One other thing Fannie Mae needs to make a MHC loan…

Mobile home park DEALS!

Deal-flow has felt damn near non-existent vs. the boom times of 2021.

Thankfully, deal flow is starting to surface. The bid-ask spread on pricing is narrowing. This is partly due to rates decreasing and partly due to seller capitulation.

Divorces and deaths are still happening and sellers are starting to realize we’re not going back to a zero percent interest rate world.

Consequently, I (and our good friend Fannie) expect many more transactions in 2025.

Happy trails,

MHP Weekly