Debt Markets - Who Turned off The Spigot?

It’s been quite the year for capital markets. In fact, it’s probably been one of the most volatile years since the great recession over a decade ago.

What began with a black swan event in 2020, has resulted in the Fed’s attempt to cool off prices by jacking rates 75 bps at a time, and they’re clearly not done yet.

It turns out cheap debt is a drug, and we're all addicted. We may not see those sub 4 percent interest rates for a while, but in the meantime properties are still trading; they’re just harder to get done.

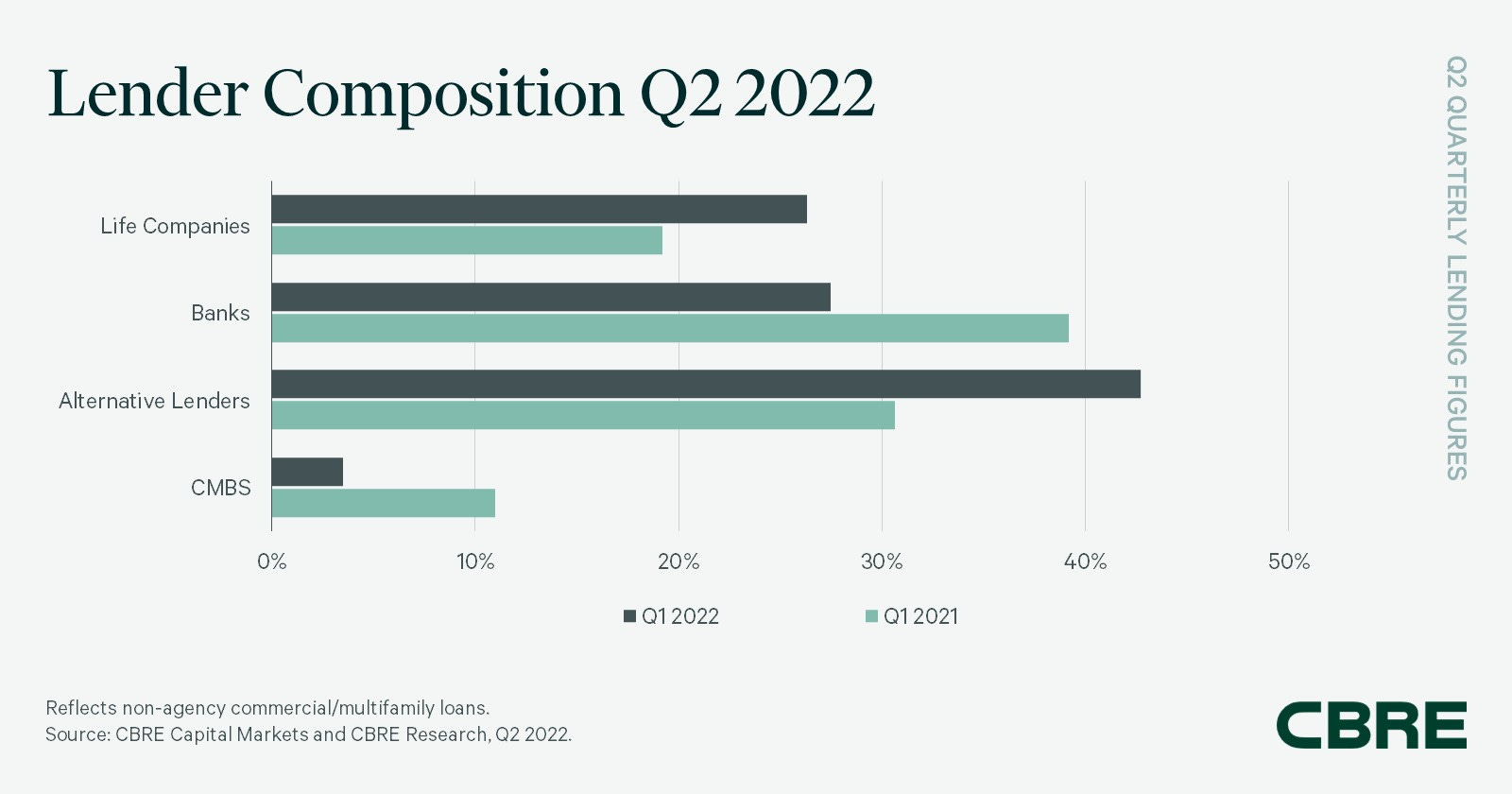

CMBS (Commercial Mortgage Back Securities) debt volume has fallen off a cliff. When you hear “pencils are down”, this is what they mean:

CMBS lenders usually free up lending capacity by offloading the lower risk “A” slice of the loan pool and keep the higher yielding / higher risk “B” piece. As these lenders don’t have a functioning market to offload loans, they are stuck holding loans on their balance sheet. This is one of the main reasons they’ve pulled out of the market (they don’t want to be balance sheet lenders).

Stepping In

Life Companies and private lenders (who are licking their chops) are starting to wade in to fill the void.

Alternative Lenders

The graphic above shows alternative lenders are taking almost 45% of the lending activity, up over 10% from Q2 2021.

This might include lending arms of private equity or hedge funds, hard money lenders, or frankly any Tom, Dick or Harry.

NOTE: If you take a private loan, tread carefully. PE firms play to win. They might be actively hoping for a default so they can step into the asset at low basis.

Shop Local

Community & regional banks are still lending, just selectively. They are loving the spike in rates, but are wisely picking their spots. They are primarily focusing on existing relationship borrowers. If you aren’t one of these borrowers, you should hire a top producing mortgage broker. They have some leverage with lenders they’ve done a lot of business with.

Don’t hesitate to dial up the local bank in the asset’s hometown. The President of the Bank might know the asset and therefore, might be more willing to work with first time borrowers.

Agency

Thankfully, agency lenders expect Fannie Mae and Freddie Mac will be active in 2023.

On Nov. 10 the Federal Housing Finance Agency set the Agencies purchase caps for 2023 at $75 billion each, down from this year’s $78 billion apiece. This is good news for price stability, bad news if you were hoping for a sea of fire sales.

We hope manufactured housing gets a healthy chunk of that $150B+ volume.

Happy Trails,

MHP Weekly