The mobile home park business looks a lot different after a decade of private equity and BiggerPockets Bros piling in.

10-15 years ago the majority of mom & pop sellers didn’t know the real potential (future value) of their property.

You consistently made money the day you bought a park.

Buy on the cheap, pass out a rent increase, sub-meter the water, enforce the park rules and boom, business plan achieved.

Hell, you didn’t even need to bump rents much.

Why?

Cheap Debt and Cap Rate Compression

Our sleepy little asset class went from shunned, to beloved.

The figure above shows how the average cap rate for MHCs compressed 200-300 basis points from 2013-2022.

The CoStar cap rates (blue line in the chart above) include all park transactions in their database - many of which are small 2 star parks in rural markets. Hence the 6.75% cap vs. 5% cap rate delta.

This cap rate compression was a gift from the Gods. Sweet Manna from heaven. It was the Red Bull that gave us wings.

Oh how I miss it so.

And if you could combine it with:

modest rent growth

operating leverage (higher portion of expenses are fixed vs. variable)

and a refinance that returned your equity...

Whammy, stellar returns.

This worked in just about every market. You still had to be good at operations, but you didn’t need to be great.

Those days are probably over.

Cap rates have lost gravity.

Interest rates are no longer pulling cap rates lower.

Better is Best

If you’ve read this newsletter awhile you’re likely sick of us talking about investing in above average markets.

But the benefits of that approach are pretty clear today.

The cap rate data above shows that institutional quality park values are holding up much better relative to lower tier parks and markets.

In fact they seem to have stabilized in 2024.

Exhibit A:

Ummm, $140K / pad, 3.6% cap seems like a pretty healthy price.

Perhaps too healthy but maybe there is a path to growth. Or maybe the buyer has long-term capital and are ninja operators that can still make the math work over 10+ years.

However, there is definitely not enough margin for error in that pricing if the team can barely operate it’s way out of a paper bag.

Because even minor slippages on collections or expenses are magnified on a deal like this.

Operations is the Way

So what happens when you can’t rely on cap rate compression or cheap debt?How do you still drive returns?

You have to be a killer operator.

Consistent and thoughtful rent bumps, expense trimming, and stellar sales & marketing.

Just ruthless execution day in and day out.

You need things to be dialed:

Talented and motivated team

Good systems & consistent communication

High touch property management

Responsive eviction process

Aggressive MHP rehab teams

Ample capital reserves

Those that don’t will end up selling to those that do.

Ultimately this is good for the industry. It needs execution to improve in order to have a functioning asset class that lifts the overall appearance, lot rents and valuations of all parks.

The industry needs to level-up with professional operations.

That’s the only way cap rates can stay low and still generate acceptable returns.

Thankfully there is a roadmap.

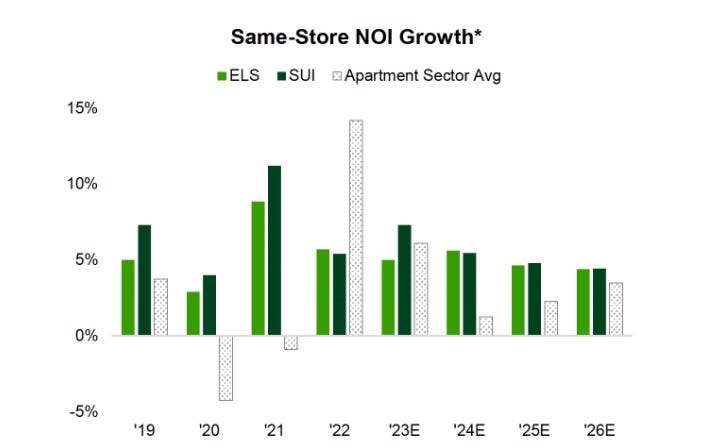

The biggest park owners have been thriving on incremental (but consistent) NOI improvements for decades by tripling down on operations.

As you likely know, Equity Lifestyle & Sun Communities push NOI growth higher EVERY. SINGLE. YEAR. averaging 5-6% as of late.

It’s not sexy, high-octane growth and its no longer an easy arbitrage cap rate play.

But if you know how to operate, buying parks is still a smart, lower risk way to invest for long-term returns.

Happy Trails,

MHP “WEEKLY”